The GDP Arithmetic

Chief Economist Scott Brown discusses current economic conditions.

Real GDP was reported to have fallen at a 32.9% annual rate in 2Q20. Nobody should have been surprised by that. Component data had already indicated massive and broad-based weakness and most economists’ estimates fell in the -30% to -35% range. News reports had generally implied that the downturn was ongoing. That’s clearly not that case, as most data reports show that economic activity bottomed out in April and growth resumed in May and June. Barring a sharp retreat in August and September, consumer spending figures point to a record pace of growth in 3Q20. Still, as Fed Chair Powell noted in his post-FOMC press conference, “Even with the improved economic news in May and June, overall activity remains well below its level before the pandemic.” The path forward depends on the virus, the efforts to contain it, and the amount of fiscal support.

GDP is a quarterly figure, but one that often depends on the months leading into it. The economy was growing nicely in January and February, but March weakness was enough to push 1Q20 GDP growth into negative territory. April was a disaster, but the March drop contributed significantly to the second quarter’s weakness. Adjusted for inflation, consumer spending fell at a 34.6% annual rate in 2Q20. The gains in May and June imply that consumer spending will rise at a record pace in 3Q20. If we were to get no monthly growth in the quarter – that is, spending remains at the June level in July, August, and September – consumer spending will have risen at a 26.8% annual rate. With COVID-19 cases rising in many states, we could see a retrenchment in spending, relative to June. However, it’s unlikely that we’ll return to a full lockdown.

Some of the May/June strength may reflect the satisfaction of pent-up demand. Consumers who were unable to spend in March and April may have bought in May and June. If that’s the case, then we may see some roll back in spending in the third quarter. Adjusting for inflation, consumer spending on motor vehicles rose 8.8% in June, up 11.7% from a year earlier. Rebounds were also strong in other consumer durables and in clothing. With consumer spending restrained by social distancing, checking and savings accounts generally grew in March and April. This may have provided a down payment on a new car, truck, boat, or Jet Ski. With most individuals still reluctant to get on a plane or go to an amusement park, families can be expected to opt for vacations a little closer to home, say a trip to the lake or shore – and wouldn’t a new car be nice?

Consumer services were hit hard in March and April. Restaurants and air travel have picked up from the April lows. Routine healthcare visits have risen following cancellations in March and April. However, consumer spending in these areas remains far below where we were in February and without a vaccine, air travel isn’t going to return to pre-pandemic levels anytime soon.

As expected, the Federal Open Market Committee left short-term interest rates unchanged after the July 28-29 policy meeting. The policy statement was a near photocopy of the one in June. One phrase was added: “The path of the economy will depend significantly on the course of the virus.” That’s fine, but Chair Powell was more cautious in his post-meeting press conference. “fter declining gradually from a peak near the end of

pril, the number of COVID-19 cases has increased sharply in many parts of the country since mid-June,” he noted, “we have thus entered a new phase in containing the virus, which is essential to protect both our health and our economy.” Powell said that the path of the economy is “extraordinarily uncertain and will depend in large part on our success in keeping the virus in check.” Unfortunately, “we have seen some signs in recent weeks that the increase in virus cases and the renewed measures to control it are starting to weigh on economic activity.”

The Conference Board’s Consumer Confidence Index and the University of Michigan Consumer Sentiment Index both dipped in July and the reports took note of a pandemic-related decrease in expectations. Consumer attitude measures do not necessarily drive spending, but are indicative of general pressures on the household sector.

The May/June improvement in consumer spending might retreat somewhat, reflecting the satisfaction of pent-up demand or an impact from rising COVID-19 cases. However, while some states have throttled back plans to re-open, we are unlikely to return to more extreme social distancing.

Monetary policy has helped to ensure adequate liquidity in the financial system, but cannot do a lot for the economy in the short-term. In his press conference, Powell said that “The fiscal policy actions that have been taken thus far have made a critical difference to families, businesses, and communities across the country,” adding that “The path forward will also depend on policy actions taken at all levels of government to provide relief and to support the recovery for as long as needed.”

Recent Economic Data

Durable goods orders rose 7.3% in June, following a 15.1% rise in May, boosted by a sharp rise in motor vehicles (which more than offset further aircraft order cancellations). Consumer attitude measures showed pandemic-related declines. The Pending Home Sales Index rose 16.6% in June, up 6.3% from a year earlier. The Employment Cost Index rose 0.5% over the three months ending in June, up 2.7% year-over-year.

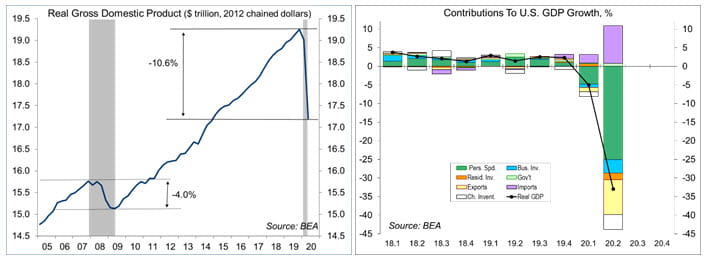

Real GDP posted a record decline in the advance estimate for 2Q20 (a -32.9% annual rate). The level was 10.6% lower than in 4Q19. In comparison, GDP fell 4.0% in the 2008-2009 financial crisis and that took six quarters.

Click here to enlarge

Click here to enlargeSecond quarter weakness was widespread across GDP components, but was especially pronounced in consumer services, transportation equipment, and energy exploration. The pandemic had an outsized impact on foreign trade (the drop in imports adds to GDP growth). Inventories also fell sharply.

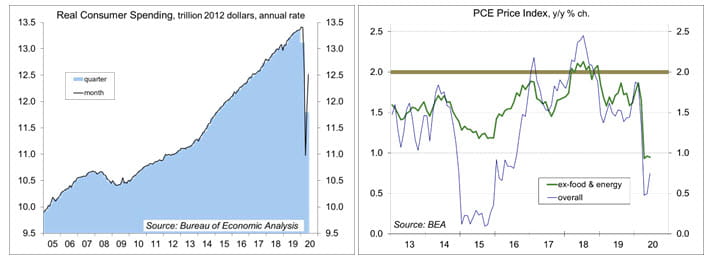

Personal income figures were mixed in June, with a further rebound (though partial) in wage and salary income. Unemployment benefits continued to rise, but government transfer payments fell (as “recovery rebate” checks and deposits went out in April and May). Adjusting for inflation, consumer spending rose 5.2% in the initial estimate for June, following an 8.4% rise is May (-5.5% y/y). Even though May and June are in 2Q20, the increases imply that spending will post a strong gain in 3Q20.

Click here to enlarge

Click here to enlargeThe PCE Price Index rose 0.4% in June (+0.8% y/y), reflecting higher prices in food and gasoline. Ex-food & energy, the PCE Price Index rose 0.2% (+0.9% y/y, vs. the Fed’s goal of 2.0%).

Gauging the Recovery

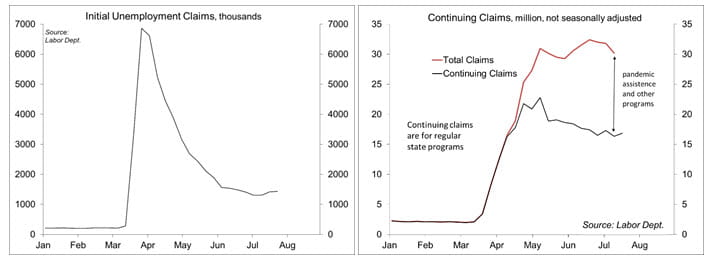

Jobless claims edged up to 1.434 million in the week ending July 25, still very high, suggesting ongoing labor market weakness. Continuing claims rose by 867,000 in the week ending July 18, to 17.018 million (seasonally adjusted). The figures are for regular state unemployment insurance programs and do not include pandemic assistance and other programs. Total recipients, including all programs, were 30.202 million (not seasonally adjusted) for the week ending July 11 (down from 31.804 million in the previous week). Pandemic assistance includes self-employed and part-time workers (who normally wouldn’t qualify for benefits), as well as individuals who had previously exhausted their unemployment benefits.

Click here to enlarge

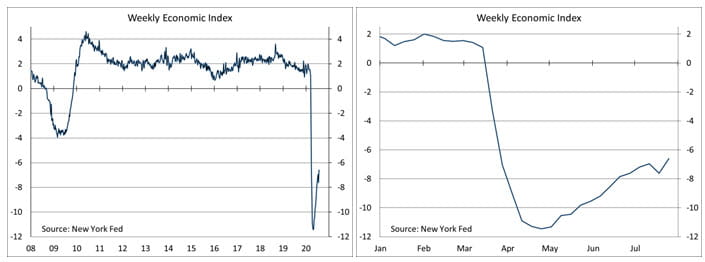

Click here to enlargeThe New York Fed’s Weekly Economic Index rose to -6.60% for the week of July 25, up from -7.24% in the previous week and a low of -11.48% at the end of April. The WEI is scaled to four-quarter GDP growth (for example, if the WEI reads -2% and the current level of the WEI persists for an entire quarter, we would expect, on average, GDP that quarter to be 2% lower than a year previously).

Click here to enlarge

Click here to enlargeThe University of Michigan’s Consumer Sentiment Index fell to 72.5 in the full-month assessment for July (the survey covered June 24 to July 27), down from 73.2 at mid-month and 78.1 in June. The report noted that “consumer sentiment sank further in late July due to the continued resurgence of the coronavirus” and cautioned that “the lapse of the special jobless benefits will directly hurt the most vulnerable and spread even further by missed rent, mortgage, and other debt payments.”

The opinions offered by Dr. Brown should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates (RJA) at this date and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the foregoing report is accurate or complete. Other departments of RJA may have information which is not available to the Research Department about companies mentioned in this report. RJA or its affiliates may execute transactions in the securities mentioned in this report which may not be consistent with the report's conclusions. RJA may perform investment banking or other services for, or solicit investment banking business from, any company mentioned in this report. For institutional clients of the European Economic Area (EEA): This document (and any attachments or exhibits hereto) is intended only for EEA Institutional Clients or others to whom it may lawfully be submitted. There is no assurance that any of the trends mentioned will continue in the future. Past performance is not indicative of future results.