GDP

January 29, 2021

Chief Economist Scott Brown discusses current economic conditions.

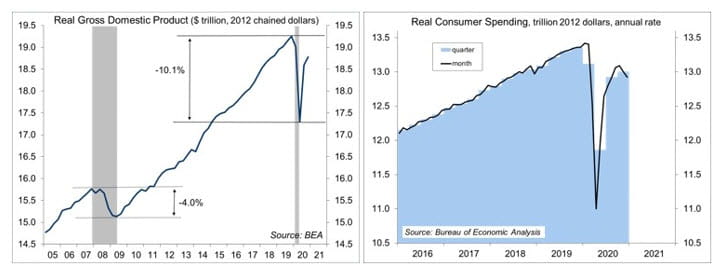

Real GDP rose at a 4.0% annual rate in the advance estimate for 4Q20, a much more moderate pace of recovery than was seen in the third quarter. Details were mixed, but consumer spending showed a significant loss of momentum and monthly figures reflected weakness in November and December. The surge in the pandemic and efforts to contain it dampened holiday sales and travel. This may, in turn, give way to seasonally adjusted strength in 1Q21, as there should be less of a fallback in the unadjusted data. However, as the Federal Open Market Committee noted in its January 27 policy statement, “the path of the economy will depend significantly on the course of the virus, including progress on vaccinations.”

Inflation-adjusted consumer spending (68% of GDP) rose at a 2.5% annual rate in the fourth quarter, down 2.6% from 4Q19. Business fixed investment (13% of GDP) rose at a 13.8% pace, down 1.3% y/y, with strength in equipment. Residential fixed investment (homebuilding and improvements, now 4.6% of GDP) rose at a 33.5% annual rate, 13.7% higher than a year ago. These three components make up Private Domestic Final Purchases (PDFP, equivalently, this is GDP less government, inventories, and foreign trade). PDFP, a better measure of underlying domestic demand, rose at a 5.6% annual rate in 4Q20, down 1.7% y/y.

Click here to enlarge

Click here to enlargeAdjusted for inflation, consumer spending on services rose at a 4.0% annual rate in 4Q20, but was still down 6.8% from a year earlier (transportation services -32.0% y/y, recreation services -41.3% y/y, and food services and accommodations -27.3% y/y)). While businesses have generally adapted to life under the pandemic, the industries that were hit the worst remain depressed. Recovery will depend on the willingness of people to get on an airplane, stay in a hotel, and go out to dinner. A quicker roll out of vaccines will get us there sooner, but there is also a risk that vaccines will be less effective against new strains of the virus. Booster shots may be needed.

One of the lessons of the 1918 pandemic is that activity will increase sharply when the current pandemic is done. We can expect a sharp recovery in travel, tourism, and in-person entertainment in the second half of this year and into 2022, although the virus and vaccinations make the timing uncertain.

Some of the pandemic strength in consumer goods may fade as spending on services picks up. Spending on consumer goods picked up during the initial part of the recovery, partly reflecting the fact that consumers couldn’t spend on services and had more disposable income. Fiscal support helped, as did the shift to working from home (which drove demand for furnishings). Inflation-adjusted spending on consumer goods fell at a 0.4% annual rate in 4Q20, while the monthly data show that weakness was concentrated in November and December.

Further fiscal support would be helpful, but there may be difficulties in getting it through Congress and requested amounts are likely to be scaled back. Monetary policy will remain accommodative until the Fed is close to its goals, which is still a long way off.

Recent Economic Data

The Federal Open Market Committee left the target range for the federal funds rate at 0-0.25% and maintained the monthly pace of asset purchases (at $120 billion per month). The policy statement was little changed from December’s, except for the acknowledgement that the pace of recovery has moderated and that the economic outlook depends on vaccinations (as well as the virus). In his press conference, Chair Powell played down concerns about possible asset bubbles and higher inflation.

Real GDP rose at a 4.0% annual rate in the advance estimate for 4Q20.

Click here to enlarge

Click here to enlargePersonal income rose 0.6% in the initial estimate for December, while figures for October and November were revised down. Personal spending fell 0.2 (-2.0% y/y), following a 0.7% decline in November (revised from - 0.3%).

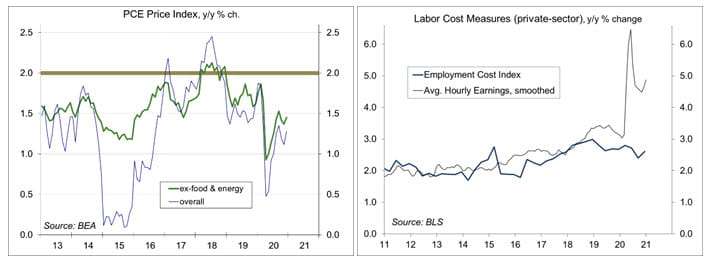

The PCE Price Index rose 0.4% in December (+1.3% y/y), led by an 8.2% jump in gasoline (-15.2% y/y). Ex-food and energy, the PCE Price Index rose 0.3%, after being unchanged in October and November (+1.5% y/y, vs. the Fed’s long-term goal of 2%).

Click here to enlarge

Click here to enlargeThe Employment Cost Index rose 0.7% (more than expected) in the three months ending in December, up 2.5% from a year ago (vs. +2.7% in the 12 months ending December 2019). The Federal Reserve looks to the ECI a better measure of labor cost pressures. Average hourly earnings can be distorted by compositional changes (such as large job losses in lower-paying industries).

Gauging the Recovery

The number of new daily COVID-19 cases has declined from recent highs, but remain elevated. Increased social distancing, whether state mandated or voluntary self-preservation, should slow the pace (and the economy) in the near term. The number of U.S. deaths from the coronavirus now exceeds 425,000.

Click here to enlarge

Click here to enlargeThe New York Fed’s Weekly Economic Index fell to -2.28% for the week ending January 23, down from -1.99% a week earlier (revised from -1.98%) and a low of -11.45% at the end of April. The WEI is scaled to four- quarter GDP growth (for example, if the WEI reads -2% and the current level of the WEI persists for an entire quarter, we would expect, on average, GDP that quarter to be 2% lower than a year previously).

Jobless claims fell to 847,000 in the week ending January 23 (873,966 before seasonal adjustment), still very high by historical standards. The high level reflects multiple filings.

Click here to enlarge

Click here to enlargeThe University of Michigan’s Consumer Sentiment Index edged down to 79.2 in the mid-month assessment for January (the survey covered January 2-13, vs. 79.2 in mid-January and 80.7 in December. The report noted “only relatively small variations since the pandemic started.” Despite the narrow range, there’s a lot of politics under the surface. For Democrats, expectations jumped to 91.8 in January from 68.6 in October. For Republicans, expectations plunged to 51.4 in January from 96.4 in October. Independents were in the middle.

The opinions offered by Dr. Brown are provided as of the date above and subject to change. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your financial advisor or use the convenient Office Locator to find our office(s) nearest you today.

This material is being provided for informational purposes only. Any information should not be deemed a recommendation to buy, hold or sell any security. Certain information has been obtained from third-party sources we consider reliable, but we do not guarantee that such information is accurate or complete. This report is not a complete description of the securities, markets, or developments referred to in this material and does not include all available data necessary for making an investment decision. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Investing involves risk and you may incur a profit or loss regardless of strategy selected. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.